special report

Crop Report 2025

Another volatile year awaits

in the feed ingredient market

Corn planted acreage Is projected to be up 5% from 2024, and soybean acreage is down 4% from last year.

By Dan Emery

In the ever-evolving landscape of global agriculture, there is a significant shift in the grain market. The agricultural commodity markets are experiencing a period of volatility, with corn futures and soybean production forecasts taking center stage. Recent US Department of Agriculture crop estimates have sparked a considerable movement in grain prices, while weather conditions continue to play a pivotal role in shaping market trends.

The market is truly global. One hiccup in any major crop-producing region of the world can result in a significant market shift. There will certainly be winners and losers. However, it is too early to tell who will fall in each category. The uncertainty continues to make the market extremely nervous. Many European protein producers feed wheat instead of corn because of local supply availability. Instability in this region will affect wheat more than corn and soybeans. Demand for soybeans continues to grow around the globe, with soybean acres planted increasing in numerous countries including record soybean production from Brazil. US exports to China will continue to be an issue, and products from Brazil will fill the void. Expect continued trade instability for the remainder of 2025 as the Trump administration attempts to level the playing field globally.

Growing conditions in the US look very favourable.

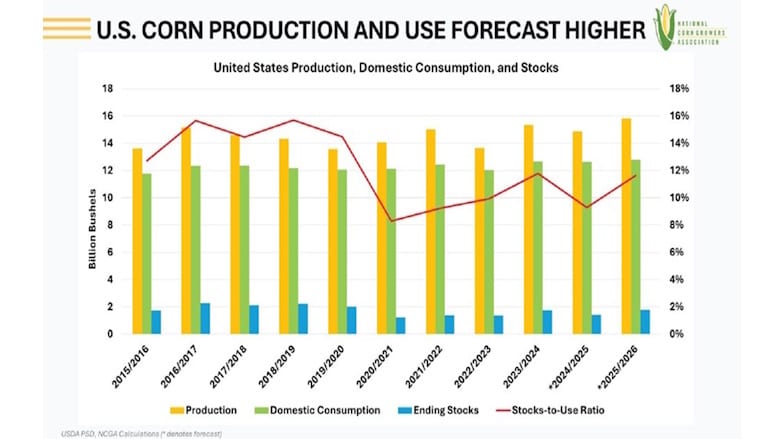

Corn planted acreage Is projected to be up 5% from 2024, and soybean acreage is down 4% from last year. USDA's National Agricultural Statistics Service estimated 95.2 million acres of corn planted in the US for 2025, up 5% from last year, according to the acreage report released June 30, 2025. Soybean area planted is estimated at 83.4 million acres, down 4% from last year. NASS surveyed approximately 67,700 farm operators during the first two weeks of June 2025 to gather information on what farmers planted.

Key findings released in the acreage report

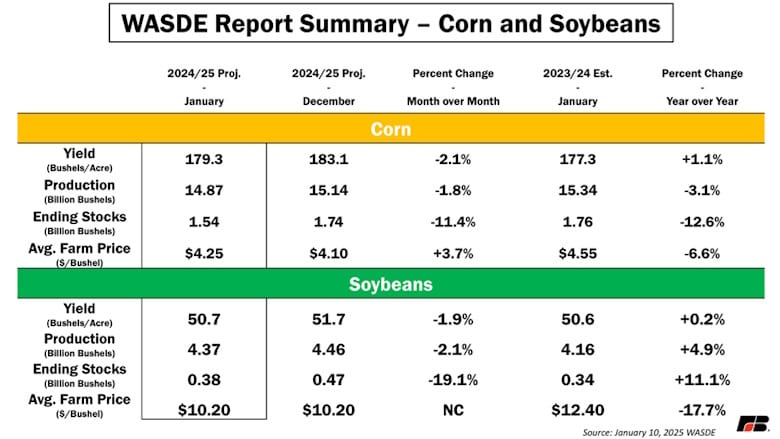

Corn: Growers expect to harvest 86.8 million acres of corn for grain, up 5% from 2024. Ninety-four percent of all corn acres planted in the United States are biotech varieties, the same as in 2024. Corn stocks totalled 4.64 billion bushels, down 7% from the same time last year. On-farm corn stocks were down 16% from a year ago, and off-farm stocks were up 6%. Corn futures have shown remarkable resilience in recent trading sessions. Corn had recently dropped to $4.20 per bushel. Strength in corn prices can be attributed to growing concerns about dry weather conditions in Argentina, the world’s third-largest corn exporter. The Rosario grains exchange has revised its 2024-25 harvest estimation downward from 51 million metric tons to 48 million metric tons, reflecting the adverse impact of weather on crop yields. This uncertainty continues to support bullish sentiments in the corn market. With Argentina facing production challenges due to dry weather, there are growing concerns about global corn supplies. This situation could potentially lead to increased demand for corn exports from other major producers, such as the US and Brazil.

Soybeans: Harvested area for 2025 is estimated at 82.5 million acres, down 4% from last year. Soybeans stored totalled 1.01 billion bushels, up 4% from June 1, 2024. On-farm soybean stocks were down 12% from a year ago, while off-farm stocks were up 18%. Stocks: The USDA’s projections for ending stocks, which represent the amount of grain left over at the end of the marketing year, have also influenced market dynamics. Tighter-ending stocks typically lead to higher prices due to supply concerns. USDA forecasts predict record Brazilian soybean harvests, causing futures to decline in recent trading. Soybeans: Record Brazilian Production Weighs on Prices In contrast to corn, soybean futures have experienced a significant decline. The most active soybean contract dropped. This downturn is attributed to market anticipations of record soybean production from Brazil, the world’s leading producer of soybeans. It is important to note that soybean prices had recently dropped to $10.20. This change, influenced by USDA downgrades and a rally in soyoil prices linked to potential modifications in US biofuel policies.

Wheat: All wheat planted area for 2025 is estimated at 45.5 million acres, down 1% from last year. Winter wheat planted area is estimated at 33.3 million acres, down less than 1% from 2024. The other spring wheat planted area is estimated at 10.0 million acres, down 5% from 2024. Other Spring planted area is estimated at 2.11 million acres, up 2% from last year. All wheat stored totalled 851 million bushels, up 22% from a year ago. All on-farm wheat stocks were up 32% from last year, while off-farm stocks were up 20%. All wheat stored totalled 851 million bushels, up 22% from a year ago. Durum wheat stored totalled 27.9 million bushels, up 32% from June 1, 2024. On-farm stocks of Durum wheat were up 41% from June 1, 2024. Wheat futures have also seen a decline. The wheat market is currently grappling with lackluster demand, which is putting downward pressure on prices.

Supply outlook

There are long-term concerns about farmers’ ability to continue supplying the feed ingredients producers need on a cost-effective basis. It is projected that around 70% of US farmland will change hands in the next 15 to 20 years, primarily due to the aging farmer population and a lack of next-generation successors for many family operations. Venture capital has been a major buyer of farmland and has consolidated operations in some areas. Additionally, experts are genuinely concerned that we continue to lower our water tables and 10 years from now will have significant challenges with the water supply and quality. Some areas of the US are facing significant water stress such as Nebraska, Colorado, California, Delaware, Ohio, Virginia, North Carolina, Arkansas and the entire Southwest.

Global background

Feed ingredients are a global topic. China consumes billions of tons of feed grains, rendering protein, materials used in agriculture, and protein. Whether these are supplied by Brazil, Australia, the US, or other sources they still offset global supply. Ukraine and Russia are also significant sources of global wheat supplies that may be displaced. Ongoing trade wars around the globe may also move some of the puzzle pieces around but people will find a source from some other part of the world. This may negatively affect US farmers.

If you follow a five-year trend, grain-based feed ingredients, including corn, wheat, and soybeans, prices travel within a pricing range of one another. Their price also correlates with the price of oil. Estimating and reducing costs is always a key factor in determining a company's success or failure in the protein business. Ethanol production continues to get more efficient, maximizing the energy extracted from every bushel of corn. Ethanol is now the number one consumer of corn with animal feed ingredients close behind.

Dan Emery is president of Meaningful Solutions.

Opening image credit: Getty Images / fotokostic / Getty Images Plus